Economic Growth For A New Era

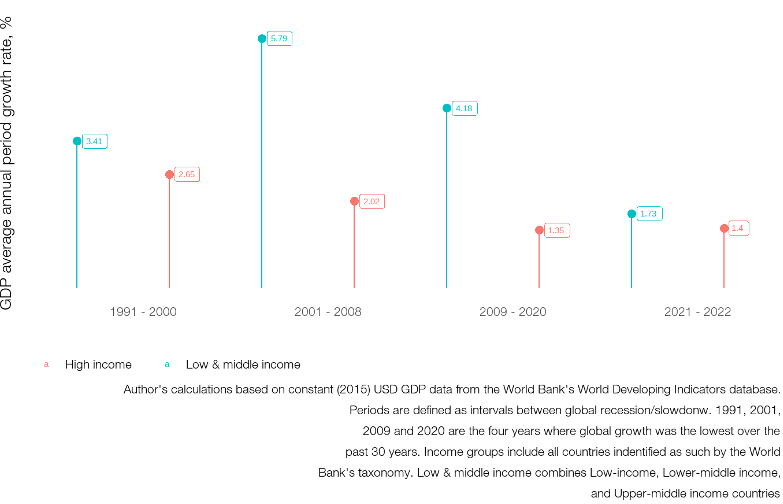

Economic Growth For A New Era(Yicai) Jan. 12 -- Since the 2007-08 financial crises, global growth has lost momentum. On average, GDP growth has declined from more than 2% in advanced economies and nearly 6% in emerging and developing economies in the early 2000s to less than 1.5% and less than 2% in the post-COVID period.

This global slowdown comes at a time when the World Bank estimates that global long-term potential output growth rates—effectively the world economy’s “speed limit”—is set to fall to a , and no more than 4% for developing economies. This is particularly bad news for that were previously on track to close at least some of the gap in income levels and standards of living to advanced economies, but who now barely grow faster, and in some cases actually more slowly, than their richer peers.

This sustained slowdown in growth has been compounded by a succession of crises. It is now more than 15 years since the beginning of the global financial crisis, yet it continues to cast a shadow, not least in the policy choices of many advanced economies. The COVID-19 pandemic, and the shock of lockdowns, left behind an aftermath of a surge in public debt levels and reversal of global development progress. Geopolitical tensions and conflicts have further reshaped an international order increasingly multipolar, with far reaching implications for technology, growth and development. Overshadowing these developments is the growing awareness that the world’s rising temperature poses grave dangers to the long-term prospects for humanity, with the world currently on track for a temperature rise significantly above the targets set out in the Paris Agreement in 2015.

These crises have raised questions not just about the wisdom of prevailing approaches to stimulating economic growth, but about the very goals and values underpinning it.

The extent to which there was previously agreement on these matters should not be overstated, with older prescriptions for growth, including the so-called “Washington consensus”, having broken down before the global financial crisis had erupted. But the forces of change have intensified over the past two decades, in particular as politics in many advanced economies has fractured, as the power and resources of emerging economies have increased, and as many leaders across the world have sought to strengthen national economic policymaking as a counterweight to the political and economic effects of globalization.

Reigniting global growth will be essential to addressing these looming challenges, including eradicating poverty, reducing inequality and tackling climate change. In a growing economy it is easier to allocate resources to competing demands than it is in a stagnant one. Yet a short-term focus on growth at all costs has in the past itself contributed to environmental damage, exacerbated inequality, and stripped out resilience safeguards in pursuit of maximum efficiency.

The question is not whether the world needs more growth, but the extent to which the underlying nature of the growth that is needed can also advance other important priorities.

Quality and quantity?

Economic policy is an inherently normative exercise, with trade-offs and synergies driving policy choices. There will inevitably be disagreements on these normative considerations. To help respond to this context, the World Economic Forum is introducing a to help complement traditional growth metrics and develop a more holistic view of the quality of growth. It is grounded in four pillars: innovativeness, inclusiveness, sustainability and resilience.

The framework does not aim to suggest that innovation, inclusion, sustainability and resilience are the only priorities to be balanced against growth, nor that they should be prioritized equally everywhere. Different countries have different circumstances and that will lead to different conclusions on those questions. The goal of the framework is to provide a tool with which countries can explore areas to improve, trade-offs to resolve or synergies to develop.

So what does it tell us about the quality of growth?

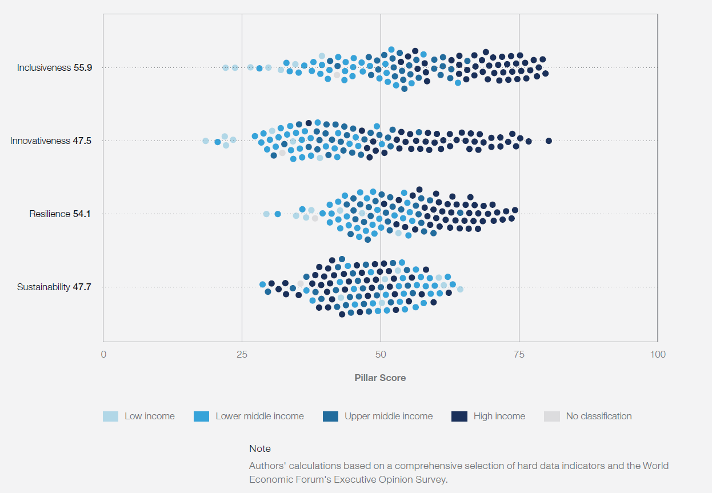

The world economy as a whole is halfway towards an ideal trajectory of fully innovative, inclusive, sustainable and resilient growth.

The innovativeness dimension, which captures the extent to which an economy’s trajectory can absorb and evolve in response to new technological, social, institutional and organizational developments to improve the longer-term quality of growth, attains the lowest global score (with a global average of 47.5 out of 100).

The sustainability dimension’s global average is 47.7 out of 100. This measures the extent to which an economy’s trajectory can keep its ecological footprint within finite environmental boundaries.

The inclusiveness pillar – which measures the extent to which an economy’s trajectory includes all stakeholders in the benefits and opportunities it creates has a global average score of 55.9 out of 100.

The resilience dimension – which captures the extent to which an economy’s trajectory can withstand and bounce back from shocks - and 54.1 out of 100, respectively.

At an individual level, no economy has attained a pillar score higher than 80 on any of the framework’s four dimensions, where 100 is the theoretical maximum outcome possible.

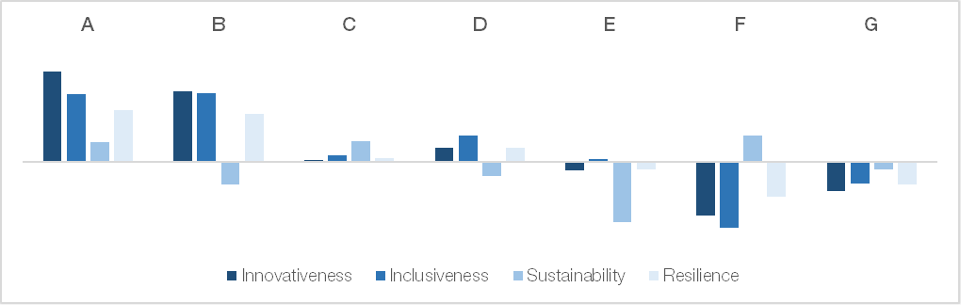

Countries differ considerably in terms of policy priorities set as well as policy implementation results. Among the 109 countries we look at, we find seven archetypes of countries that are most closely related in their growth characteristics.

The first group is generally rich countries that are leaders in inclusion, resilience, innovativeness – and putting in place measures that will make them more sustainable too. Their growth rates are under 1% but given their starting point, the absolute value of their output is high while combined with high quality. They are the closed to having found a synergistic approach to quantity and quality. This group includes Austria, Switzerland, Germany, Denmark, Finland, France, United Kingdom, Netherlands and Sweden from Europe, alongside Japan and South Korea from East Asia.

The second group is very similar in other characteristics – but lives somewhat beyond its means when it comes to sustainability, imposing a price on their future – and the planet’s. It includes Australia, Canada, and the United States.

The third group are countries with moderate but balanced growth profiles, as well as above average performance on sustainability which include Brazil, Botswana, Chile, Colombia, Costa Rica, Ghana, Italy, Jordan, Morocco, Portugal and Spain—are further characterized by moderate GDP per capita growth, averaging 1.07% over the past five years.

The fourth group are countries with comparatively high growth (between 2 and 5%) and strong economic fundamentals but still in transition to a more innovative, inclusive and resilient growth trajectory. Countries include Bulgaria, Ireland, Serbia, Greece, Hungary, Indonesia, Lithuania, Latvia, Mauritius, Malaysia, Poland, Qatar, Romania, Slovenia, Thailand, Uruguay, and the United Arab Emirates.

The fifth group are countries with traditionally resource-intensive growth, with some seeking to diversify and transform the characteristics of their growth trajectory. Countries characterized by this archetype score low on sustainability but are generally in line with global averages across the innovativeness, inclusiveness, and resilience pillars. These countries—which include Argentina, Bahrain, Kazakhstan, Kuwait, Mongolia and Saudi Arabia—are further characterized by low recent growth performance, averaging 0.01% GDP per capita growth over the past five years.

The sixth and seventh groups have poor quality growth, performing generally below average on inclusion, innovativeness and resilience. But they have one distinction – one is well above average on sustainability, while the other performs below average on all fronts.

The sixth group includes countries with traditionally efficiency-driven growth pathways, building up innovativeness, inclusiveness and resilience from a low base with comparatively low environmental footprint. They have limited technology adoption and where economic modernization has occurred it’s in a few hotspots, while most of the country remains economically underdeveloped. Countries include India, Kenya, Rwanda, Tanzania, Viet Nam, but also Nigeria, Pakistan, El Salvador, Guatemala, Nepal, Senegal and Sierra Leone. Given the wide range of countries represented by this archetype, growth rates vary significantly across countries, ranging from 5.5% GDP per capita growth in India over the past 5 years, and 3.72% in Viet Nam, to -2.5% in Pakistan or 0.3% in Nigeria.

The last group includes countries with balanced but below average innovation, inclusion and resilience profiles, with comparatively strong performance on sustainability. This includes Bangladesh, Egypt and Türkiye, with a comparatively high average GDP per capita growth of 3.34% over the past five years, and also Mexico and South Africa who saw their GDP per capita decline by -0.51% over the past five years.

A path to better growth

While each other country faces its own unique set of trade-offs and synergies to design its policy choices, there are some key takeaways that are near universal and largely have global dependencies, when it comes to technology and knowledge transfer, development aid, immigration policy, or trade and investment.

Most countries are inadequately prepared for demographic change. In high-income economies, talent availability is an increasing bottleneck to further advance innovativeness. This opens an opportunity for trade in services from developing economies that is still largely untapped, in part because of low digitalization.

Digitalization rates across advanced and developing economies are diverging rather than converging, leading to persistent economic divides and missed opportunities for innovation. Digitization – and the infrastructure and services that accompany it - for the three billion people that are not yet online is key.

Income inequality has been on the rise in recent years for the first time in decades and is currently the most evident headwind to making growth more inclusive across economies. Widespread access to basic services like health and lifelong learning, in addition to adequate social protection, will be key to inclusive growth in developed and developing economies alike.

Institutional commitments are yet to translate into systemic hardwiring of emissions reduction into growth models. Green finance and green technology are the missing links on the path to sustainability and most high- and middle- income economies are yet to take the lead.

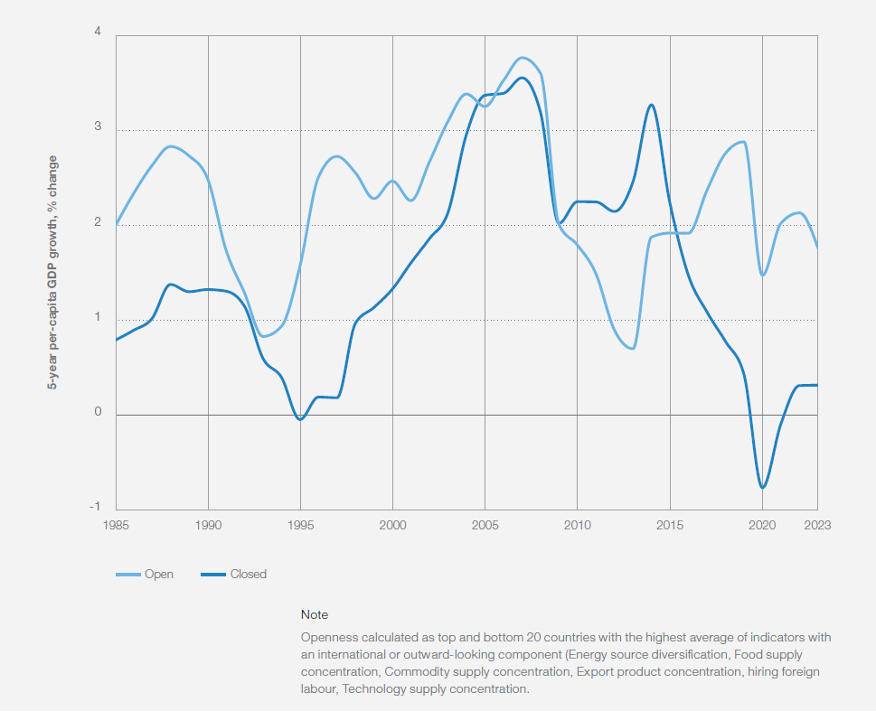

Finally, inward-looking approaches are insufficient for resilience – more open economies still have higher income per capita and bounce back better from shocks. But localized efforts such as for strengthening financial architecture, food and water security, are also key.

The World Economic Forum’s Future of Growth Initiative will lead a two-year campaign aimed at inspiring discussion and action around charting new pathways for economic growth and supporting policymakers in balancing growth, innovation, inclusion, sustainability, and resilience goals.

This new era of globally interconnected crises demands a new level of urgency and ambition on rewiring growth for a new era. Policymakers across key portfolios – finance, industry, economy, trade, planning, environment, and labour – need to take notice.

(Saadia Zahidi is a Managing Director at the World Economic Forum.)

Saadia ZahidiSaadia Zahidi is a Managing Director at the World Economic Forum.

Saadia ZahidiSaadia Zahidi is a Managing Director at the World Economic Forum.