Clean Power Across Industry is Key for China to Meet Net Zero, Two Approaches Can Accelerate Its Use

Clean Power Across Industry is Key for China to Meet Net Zero, Two Approaches Can Accelerate Its Use(Yicai Global) June 29 -- The World Economic Forum is collaborating with Accenture on the Clean Power for Industry initiative. It aims to help accelerate the transition of China’s industrial sector, through collaborative action, towards net zero to achieve sustainable development.

Background

Figure 1

Figure 1

Source: Financial Times

China's industrial sector accounts for more than half of the world's production capacity, and its final energy consumption is expected to grow rapidly, surpassing other countries. In 2020, China was responsible for 40% of global industrial carbon emissions; among them, the iron and steel and aluminum industries were the main sources of carbon emissions from electricity use in the industrial sector. In future increasing electrification and developing renewable energy will help reduce the carbon footprint of the industrial sector.

On the other hand, China's Energy Transition Index (ETI) has been on an upward trend over the past 10 years. Strong policy support and continued high levels of investment and R&D in renewable energy have boosted China's readiness for energy transition by 43% over the past decade. China has built a robust ecosystem for renewable energy manufacturing and nurtured many emerging industries. The main drivers of this are the diversification of power supply and the enhancement of grid quality. It also shows that it is time to vigorously develop clean power in industrial sector.

Mainstream solutions for developing clean power

The two main solutions for accelerating clean power deployment in the industrial sector are captive power transition and green power trading.

Key challenges and corresponding planning & opportunities

First of all, primary aluminum is one of the high-energy-consuming industries, and its coal-fired captive power capacity needs to be transferred to the southwest region rich in hydropower resources. According to our analysis and forecast, without further policy tightening, the hydropower resources in Southwest China will reach their limit for new primary aluminum capacity after 2025, so alternative clean power methods need to be explored.

Secondly, rooftop solar panels have a large potential market in China, but their installation is limited by factors such as property rights and procedures. In the future, with more policy incentives, the installed capacity and coverage of rooftop solar panels will continue to expand, and some barriers will be eased or removed.

Third, in terms of renewable energy consumption, with the progressive increase in the share of renewable energy power generation, curtailment of wind and photovoltaics (PV) needs to be reasonably evaluated and linked to market mechanisms. At the same time, the deployment of microgrids can help balance the curtailment rate of wind and PV.

Fourth, wind, PV and energy storage can benefit power producers, the grid and users, but the high cost discourages market players from investing in energy storage projects. It is important to note that the investment cost of PV is expected to decrease annually, as well as the kilowatt hour cost of energy storage equipment associated with it as utilization time increases. Compared to alternative energy storage models, shared energy storage reduces costs and increases revenues. For example, in Zhejiang Province, as a pilot, the economic efficiency of energy storage projects has been improved by implementing favorable policies ranging from the provincial to the municipal to the district and county levels, such as electricity price subsidies and investment subsidies. Currently, wind, PV and energy storage is still in the early stage of development. It is believed in the future, as technology improves and costs fall, it will have a scale effect and gradually become fully market oriented. At the same time, the deployment and popularization of microgrids can help to control the high cost of energy storage. Microgrids would gradually shift from ensuring electricity supply to generating clean energy and then to achieving zero-carbon goals, from isolated locations to developed cities, with the support of energy storage.

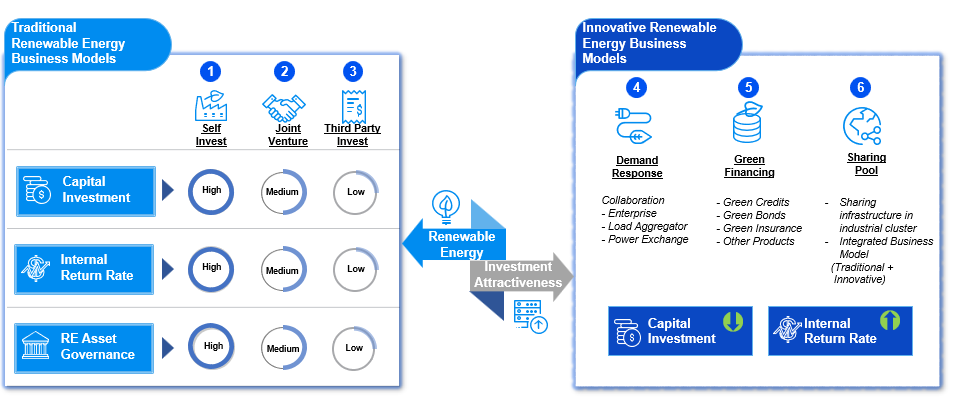

Fifth, the five major sectors in the industrial field have made significant investments in the captive power transition, and their main business models are mainly self-investment and joint ventures. As illustrated in Figure 2, most enterprises today adopt a single business model, making the return on investment unattractive. The introduction of innovative business models such as demand response, green financing, and sharing resource pools will assist companies in diversifying risks and increasing returns.

Figure 2

Source: Accenture analysis

First of all, the participants and scale of China's green power trading are still relatively limited. In the future, the model of joint procurement in upstream and downstream supply chains could foster more cross-domain collaboration and further promote the sustainable value chain for industrials. For instance, Apple jointly works with its supply chains to identify and implement opportunities and solutions for renewable energy.

Secondly, the green power price is generally higher than the average market price of conventional electricity in China. A lesson from the case of the first cross-provincial green power trading in East China Power Grid is that compared with Shanghai, Anhui and Jiangsu have relatively abundant green power resources. Delivering green electricity to Shanghai not only meets the demand for green electricity in Shanghai, but also achieves optimal resource allocation by providing more economical renewable energy power to the demand side.

However, the green power supply and demand value chain has not realized the linkage between green power and the carbon market. In the future, with the continuous maturity of policy guidance and market mechanisms, electricity-carbon coupling is just around the corner.

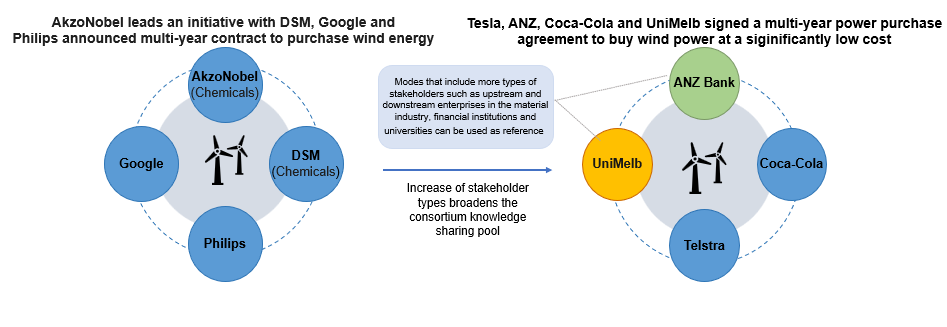

Finally, China’s green power trading in the industrial sector is still in its infancy and has not yet developed a systematic operating model and management system. Most of them focus on solving some temporary problems and isolated tasks. In fact, there are various operating modes for green power trading, such as in-house self-operation, external support and sharing resource pool. For example, BASF runs its own renewable energy business through its wholly-owned subsidiary and helps the EU achieve its carbon neutrality goal through long-term renewable energy power trading. As a professional consultant for renewable energy procurement, Schneider is committed to using its expertise and experience to provide more comprehensive consultation and advice to industrial companies and assist them in completing their green transformation. As shown in Figure 3, companies such as AkzoNobel and DSM achieved green power trading through resource sharing pool, which enabled them to access more opportunities to purchase green power, reduce electricity costs, and introduce more types of cooperation among stakeholders, and further promote the development of innovative sharing model. In the future, China's industrial sector should actively learn from advanced cases, explore the pros and cons of different models, and advance green power trading towards maturity and professionalism.

Figure 3

Source: Accenture analysis

Conclusion

Industrial decarbonization in China will play a vital role in achieving national and global carbon reduction targets. Therefore, one of the key solutions for decarbonizing industrial sector is to rapidly increase the use of clean power, which means transforming fossil fuel captive power into clean power and establishing a robust green power trading market. The continuous maturity of policies and the improvement of marketization will bring bright prospects for clean power, and industrial enterprises need to overcome existing challenges and seize new opportunities.

Roberto BoccaHead of Centre for Energy and Materials; Member of the Executive Committee, World Economic Forum

Roberto BoccaHead of Centre for Energy and Materials; Member of the Executive Committee, World Economic Forum