The competition pattern of global wind turbine manufacturers has been fully reshuffled, and Chinese enterprises have come from behind.

On March 17, the "2024 Global Wind Turbine Market Share" report released by Bloomberg New Energy Finance showed that the global installed wind power capacity was 121.6 GW last year, which was twice the level in 2019 and increased by about 3% year-on-year. Among them, the new installed capacity of onshore wind power was 109.9 GW, accounting for 90%, and the new installed capacity of offshore wind power was 11.7 GW.

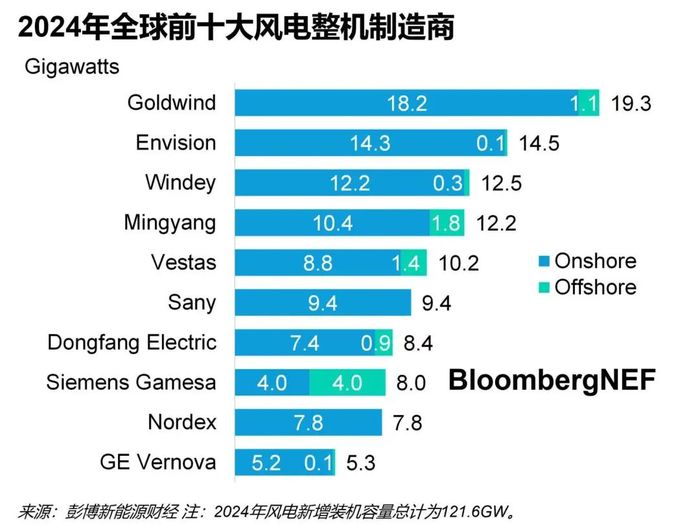

It is worth noting that in the ranking of the world's top 10 wind turbine manufacturers released by the agency last year, Chinese companies occupied six seats. The top four are for Chinese companies, the first time since Bloomberg New Energy Finance began publishing rankings in 2013. European and American manufacturers also fell out of the top three for the first time.

Last year, the world's top 10 wind turbine manufacturers were Goldwind (002202.SZ), Envision Energy, Yunda (300772.SZ), Mingyang Intelligent (601615.SH), Vestas, Sany Renewable Energy (688349.SH), Dongfang Electric (600875.SH), Siemens Gamese, Nordex and GE Vernova)。

Compared to the 2023 rankings, the top 10 participants have not changed, but a number of established foreign companies have declined in the rankings. Among them, Vestas, a Danish wind turbine manufacturer, fell two places to fifth. GE fell even more, falling four spots to tenth.

Among Chinese enterprises, Yunda shares advanced one place to the third position; Mingyang Intelligent and Sany Renewable Energy will each increase one place compared with 2023; Dongfang Electric jumped three places from 10th to 7th.

Source: Bloomberg New Energy Finance

The

ranking of Chinese wind power manufacturers released by Bloomberg New Energy Finance at the end of February is in line with the ranking of Chinese companies in the above list. In China, Goldwind occupies 22% of the market share, Envision Energy accounts for 17%, and Yunda and Mingyang Intelligent have a small gap, both around 14%.

Although Vestas's ranking has declined, its performance last year was relatively bright among foreign companies. According to the financial report, thanks to the recovery of wind turbine prices, Vestas achieved revenue of 17.295 billion euros (about 136.362 billion yuan) last year, a year-on-year increase of 12.4%; The net profit was 494 million euros (about 3.895 billion yuan), an increase of 6 times year-on-year.

In 2024, Vestas delivered a total of 12.9 GW of units, basically unchanged year-on-year, including 11.5 GW of onshore units and 1.4 GW of offshore units. At the same time, 16.9 GW of new unit orders were added, including 12.3 GW of onshore unit orders and 4.6 GW of offshore unit orders.

Tianfeng Securities recently pointed out in its analysis that in the past two years, new orders for Vestas fans have fluctuated, but the average price of fans has continued to rise. Superimposed machine enterprises naturally have the advantages of wind turbine supporting operation and maintenance services, and Vestas' fan operation and maintenance business has the growth resilience of stable revenue generation throughout the life cycle and continuous improvement of management scale.

By the end of 2024, Vestas will have an installed capacity of 155 GW of wind farms, with a revenue of 24 euros per kilowatt of operation and maintenance services in 2024, and 480 euros/kw for the whole life cycle based on 20 years, which is 40-50% of the selling price of overseas wind turbines.

Taking Vestas's 2020 data as an example, Tianfeng Securities said that the profit margin of its operation and maintenance sector is 9 times that of wind turbine sales, and the profit of operation and maintenance per GW is 3.9 times that of wind turbine sales, and if we take the data of 2019 as an example, the profit margin of the operation and maintenance sector is 3.6 times that of wind turbine sales, and the profit of operation and maintenance per GW is 1.6 times that of wind turbine sales.

General Electric, which fell the most in the ranking last year, had a total order volume of $7.1 billion in wind power business last year, down nearly 40% year-on-year.

In 2024, GE restructured its wind power business, and GE Vernova, the power and wind power business unit, was listed separately.

After Trump halted offshore wind development, GE's business strategy also shifted. The company previously mentioned that it plans to suspend new orders for offshore wind and will focus on executing existing orders and servicing existing customers.

In the field of offshore wind power, Siemens Gamesa returned to the top of the global offshore wind turbine supplier list, surpassing Vestas and Chinese companies for the first time since 2020.

Siemens Gamesa added 4 GW of installed wind power capacity last year, more than doubling year-on-year. According to statistics from Bloomberg New Energy Finance, Siemens Gamesa's offshore wind turbines accounted for nearly three-quarters of the market outside Chinese mainland last year.

Jiemian News noted that among the top ten wind power manufacturers in the world, Siemens Gamesa is also the enterprise with the largest proportion of new installed offshore wind power, reaching 50%.

In

recent years, Siemens Gamesa has been deeply affected by wind turbine quality problems, and last year, the company launched a comprehensive overhaul of its wind power sector in hopes of breaking even by 2026.

Among Chinese enterprises, Mingyang intelligent offshore wind power accounted for a relatively high proportion, and the new installed capacity of this part reached 1.8 GW last year, accounting for about 14.75%.

Image source: Bloomberg New Energy Finance

According to the "2024 Statistical Briefing on China's Wind Power Hoisting Capacity" released by the Wind Energy Professional Committee of the China Renewable Energy Society, a total of seven complete machine manufacturing enterprises in China achieved new offshore wind power installations last year, and Mingyang Intelligent continued to rank first, with a market share of about 30%, followed by Goldwind Technology and Dongfang Electric.

But Bloomberg New Energy Finance said it tracked seven companies in Chinese mainland that added a large number of new offshore wind power installations, and none of them were in a global dominant position.

According to Bloomberg New Energy Finance, the global installed capacity of offshore wind power will increase to 11.7 GW in 2024, a year-on-year increase of 6%. Among them, the new installed capacity of offshore wind power in Chinese mainland reached 6.1 GW, although it decreased by 1.6 GW compared to 2023 due to project delays, it still accounts for more than half of the new installed capacity of global offshore wind power, and is still the world's largest offshore wind power market so far.

China is also the world's largest wind power market. According to the "2024 China Wind Power Hoisting Capacity Statistical Briefing", 14,388 new wind power units were installed in the country last year, with a capacity of 86.99 GW, a year-on-year increase of 9.6%.

By contrast, outside Chinese mainland, new wind power capacity fell 10% year-on-year last year. Among them, the U.S. market shrank for the fourth consecutive year. According to the above-mentioned agency data, the new installed capacity in the United States in 2024 will only be 5.4 GW, a new low in a decade.

"U.S. project developers are hampered by slow execution, reflecting a nearly doubling of lead times, shortages of transformers and other electrical equipment, and high interest rates. Although the wind industry faces stronger political headwinds during Trump's second term, the U.S. market still has a large pipeline of projects. Bloomberg New Energy Finance believes.

Trump is inclined to traditional energy and has not been optimistic about the development of new energy industries such as wind power. On Jan. 8, Trump said at a news conference at Mar-a-Lago in Florida that he would seek a policy of not building any wind farms during his second presidential term.

On January 20 this year, on the first day of his tenure as the 47th president of the United States, Trump signed an executive order announcing the temporary withdrawal of offshore wind power leases in all areas of the outer continental shelf and reviewing the leasing and licensing of wind power projects by the US federal government.

Oliver Metcalfe, head of wind research at Bloomberg New Energy, said that during Donald Trump's presidency, offshore wind projects were more vulnerable to changes in U.S. government policy than onshore wind projects, and the onshore wind industry received more bipartisan support.

Massive information and accurate interpretation are all in the Sina Finance APP

Ticker Name

Percentage Change

Inclusion Date