(Source: Hualong Securities Research).

Xing Tian is an analyst in the machinery industry

Key takeaways:

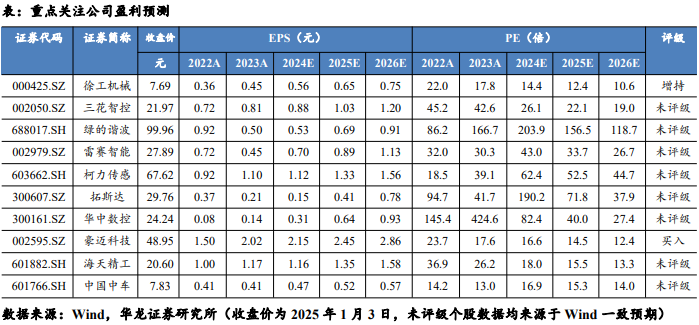

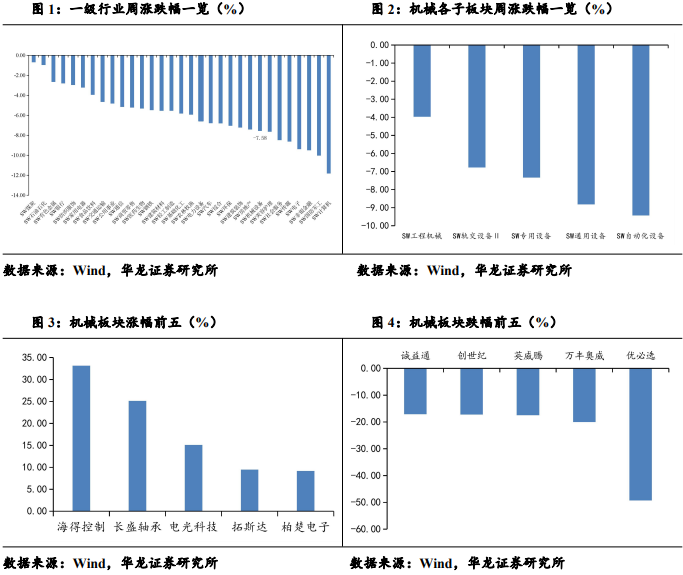

From December 30, 2024 to January 3, 2025, the Machinery and Equipment Index fell by 7.58%, ranking 24th in the primary industry classification. Affected by the overall market correction, all sub-sectors fell to varying degrees, among which construction machinery (-3.97%) and rail transit equipment (-6.78%) fell relatively little, and automation equipment with strong technological attributes (-9.43%) fell more. We believe that there are many sub-sectors in the machinery and equipment industry, and there are still structural investment opportunities, and we maintain the "recommended" rating of the industry. You can pay attention to: (1) the strategic highland of science and technology power - humanoid robots, semiconductor equipment, consumer electronic equipment, etc.; (2) Pro-cyclical sectors that benefit from the recovery of domestic demand, such as construction machinery and CNC machine tools.

CES is about to open, focusing on investment opportunities in robotics and consumer electronic devices. The 2025 CES Global Consumer Electronics Show will be held from January 7 to 10, 2025, as the world's largest, most authoritative and influential technology event, CES is known as the "Spring Festival Gala of Science and Technology", and is the vane of global technological innovation and consumer electronics industry. At that time, leading technology players from all over the world will showcase the most cutting-edge innovative technologies and excellent products, which are expected to catalyze the market of humanoid robots and consumer electronics. We believe that 2025 is the first year of mass production of humanoid robots, and the industry is expected to gradually transition from thematic investment to fundamental investment. You can pay attention to: Sanhua Intelligent Control (002050. SZ), green harmonics (688017. SH), Leisai Intelligent (002979. SZ), Keli Sensing (603662. SH), Topstar (300607. SZ) and so on.

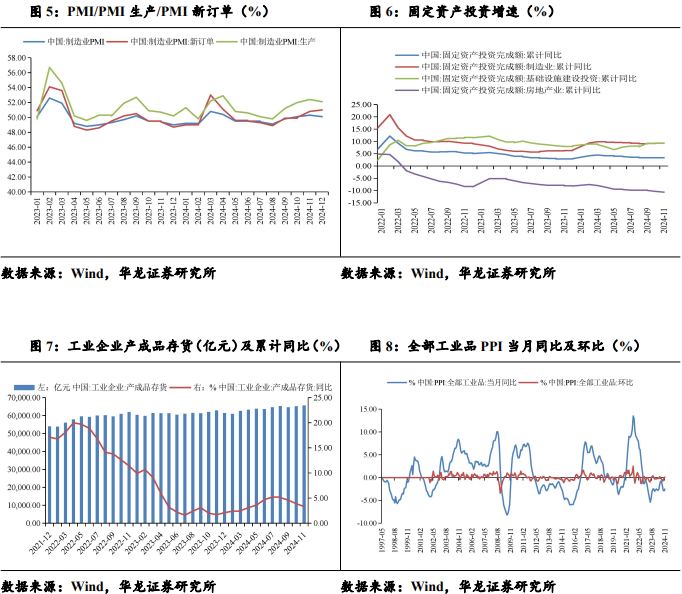

The December new orders PMI was +2.3pct YoY, focusing on the progress of the general equipment recovery. China's manufacturing PMI for December 2024 was 50.1, +1.1pct year-on-year. Among them, the production index was 52.1%, +1.9pct year-on-year, and the production index was not weak in the off-season; The new orders index was 51%, +2.3pct year-on-year, and it was in the expansion range for three consecutive months. The rebound for three consecutive months indicates that the signs of recovery from the bottom of the economy are more obvious, and the effect of incremental policies on business confidence has become stronger. Industrial machine tools are the main varieties of general equipment, which are greatly affected by policy support and macroeconomy. We believe that under the background of strong policy support, China's machine tool application scenarios are further opened, and the process of domestic substitution is expected to accelerate; Combined with large-scale equipment updates, the pro-cyclical "industrial machine tool" sector is expected to accelerate recovery. It is recommended to pay attention to: Huazhong CNC (300161. SZ), Neway CNC (688697. SH), Haitian Precision (601882. SH), Halma Technology (002595. SZ), Ou Keyi (688308. SH) and so on.

CRRC disclosed orders from August to December 2024, with a total amount of about 69.35 billion yuan. These include about 19.26 billion yuan of EMU sales contracts, about 16.9 billion yuan of EMU advanced repair contracts, about 10.4 billion yuan of urban rail vehicles and equipment sales and maintenance contracts, and about 7.07 billion yuan of freight car sales contracts. On November 13, 2024, the official WeChat account of China Railway disclosed that from January to October, the national railway completed 635.1 billion yuan of fixed asset investment, a year-on-year increase of 10.9%. From a policy perspective: On July 18, 2024, the Ministry of Transport and other thirteen departments issued a notice on the issuance of the "Action Plan for Large-scale Equipment Renewal of Transportation", pointing out seven major update actions and pointing out that 2028 is the time node for the main goal to be achieved. From the perspective of demand: On November 5, 2024, China Railway Group issued the second 350km Fuxing EMU bidding announcement, with a total of 80 units tendered, and the total number of tenders has reached 245 as of November 2024. Policies promote the release of renewal demand, and the valuation center of the industry is expected to move up. Attention: CRRC (601766. SH), China Railway Industry (600528.SH), China General Number (688009.SH), etc.

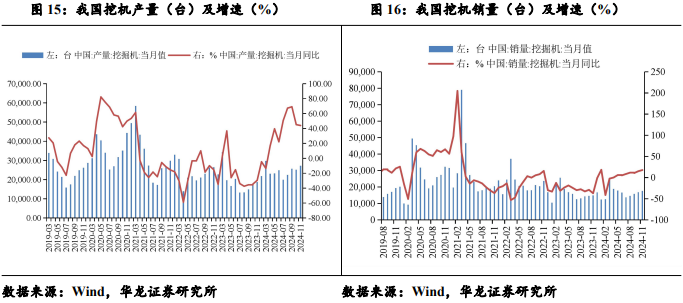

Excavator sales in November were +17.9% YoY, better than CME expectations. Among them, domestic sales were 9,020 units, a year-on-year increase of 20.5%; The export volume was 8,570 units, a year-on-year increase of 15.2%. Better than the previous CME forecast: estimated sales in the domestic market of 8,600 units, a year-on-year increase of nearly 15%; The estimated sales volume in the export market is 8,300 units, an increase of nearly 12% year-on-year. The market continued to recover, the domestic market bottomed out and rebounded significantly, and the export market gradually recovered. The domestic market has benefited from the arrival of a new round of centralized replacement cycle, the gradual emergence of the effect of real estate easing policies, and the catalytic effect of the country's large-scale replacement policies, and its growth has been relatively fast. The export market benefited from the gradual completion of the destocking of domestic brands, the low base in the same period, and the recovery of demand in some overseas areas, and the monthly sales volume returned to positive growth. Suggested Attention: XCMG Machinery (000425. SZ), Sany Heavy Industry Co., Ltd. (600031. SH), Zoomlion (000157. SZ)。

Risk warning: macroeconomic prosperity is less than expected, fixed asset investment is less than expected, raw material price increase risk, industry and market competition risk, industrial policy change risk, third-party data error risk, etc.

1. Weekly market performance

2024.12.30-2025.01.03 The machinery and equipment industry fell by 7.58%, ranking 24th out of 31 first-class industries. In the sub-sectors, construction machinery (-3.97%), rail transit equipment (-6.78%), special equipment (-7.33%), general equipment (-8.82%), and automation equipment (-9.43%).

Among the key stocks covered, the top five companies were Haide Control (+33.15%), Changsheng Bearing (+25.15%), Dianguang Technology (+15.11%), Topstar (+9.49%), and Baichu Electronics (+9.19%); The top five companies that fell were UBTECH (-49.29%), Wanfeng Aowei (-20.03%), INVT (-17.49%), Genesis (-17.24%), and Chengyitong (-17.1%).

2. Key industry data of the week

As of December 2024, China's manufacturing PMI was 50.1%, +1.1 pct year-on-year and -0.2 pct month-on-month, and it was on the boom and bust line for three consecutive months; Manufacturing New Orders PMI 51%, +2.3pct YoY and +0.2pct MoM; The manufacturing production PMI was 52.1%, +1.9 pct year-on-year and -0.3 pct month-on-month.

As of November 2024, the cumulative value of investment in fixed assets increased by 3.3% year-on-year, of which manufacturing investment increased by 9.3% year-on-year, and infrastructure investment increased by 9.39% year-on-year.

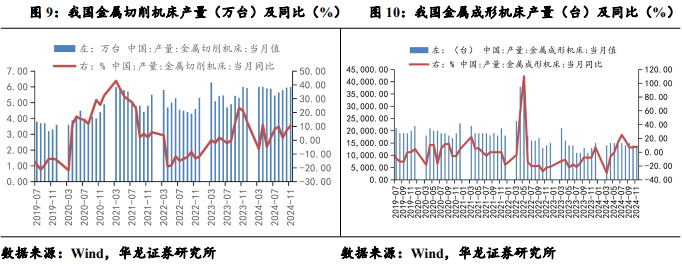

As of November 2024, the inventory of finished products of China's industrial enterprises was 6,567.08 billion yuan, an increase of 3.3% year-on-year; As of November 2024, the PPI of all industrial products in China decreased by 2.5% year-on-year and increased by 0.1% month-on-month.

In November 2024, the output of metal cutting machine tools will be 60,000 units, an increase of 10.5% year-on-year; In November 2024, the output of metal forming machine tools was 14,000 units, an increase of 7.7% year-on-year.

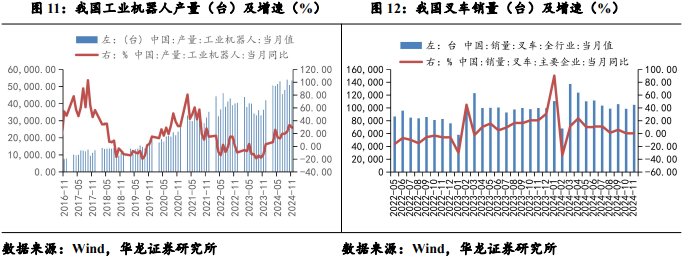

In November 2024, China's industrial robot output was 53,581 units, an increase of 29.3% year-on-year; In November 2024, 104944 forklifts were sold in China, an increase of 5.07% year-on-year.

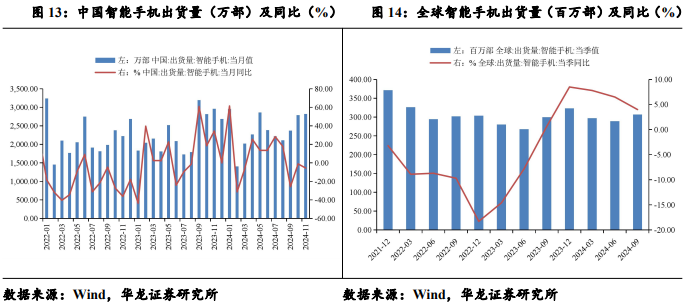

In November 2024, China's smartphone shipments were 28.193 million units, a year-on-year decrease of 5.6%; In the third quarter of 2024, global smartphone shipments reached 307 million units, an increase of 4% year-on-year, and the growth rate maintained a high growth rate for four consecutive quarters, and smartphone shipments recovered significantly.

In November 2024, China produced a total of 27,189 excavators, a year-on-year increase of 44%; In November 2024, a total of 17,590 excavators of various types were sold, an increase of 17.9% year-on-year. The growth rate of domestic sales of excavators has been positive year-on-year for eight consecutive months since it turned positive in April 2024.

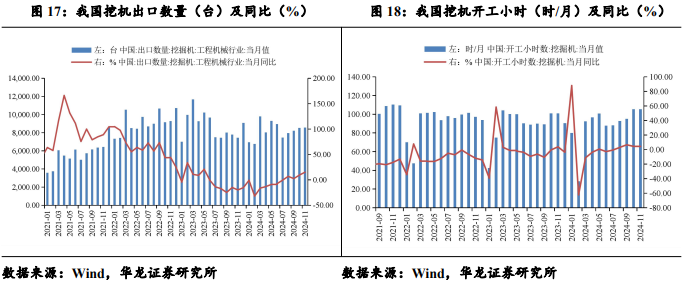

In November 2024, China exported 8,570 excavators, a year-on-year increase of 15.2%. In November 2024, the number of operating hours of excavators in China was 105.4 hours/month, a year-on-year increase of 4.4%, and the operating end recovered.

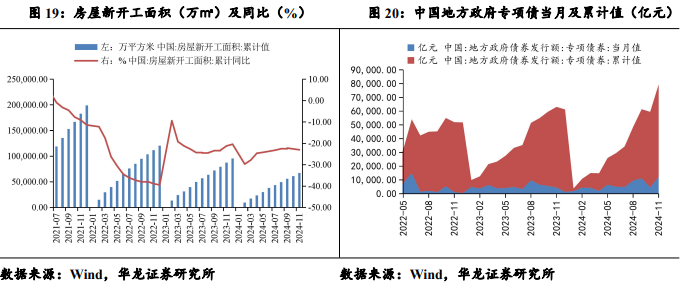

In November 2024, the total area of new real estate construction in China was 673,084,400 square meters, a year-on-year decrease of 23%; In November 2024, 1,230.7 billion yuan of local government special bonds were issued in the same month, and a total of 6,717.1 billion yuan was issued from January to November.

3. Industry news

Robots

With an annual output of 1 million humanoid robots, the industrialization project of planetary roller screw was born. On January 3, 2025, the groundbreaking ceremony of the industrialization project of Hangzhou Xinjian Electromechanical Transmission Co., Ltd. with an annual output of 1 million humanoid robot planetary roller screws was successfully held. This project not only marks a major breakthrough in the field of humanoid robots, but also demonstrates its deep accumulation and strong strength in the field of intelligent manufacturing. (China Robot Network).

BYD established a future laboratory to develop robots: focusing on embodied intelligence. According to the news of China Robot Network on January 2, 2025, BYD's 15th business division has set up a special team to develop embodied intelligence, and Luo Zhongliang, the top person in charge of the business department, is directly in charge of the project, focusing on the field of embodied intelligence, including the research and development of robots. (China Robot Network).

NVIDIA will ramp up support for robotics in 2025. According to the China Robot Network on January 2, 2025, in the first half of 2025, NVIDIA will launch a new generation of compact computers called JetsonThor for humanoid robots. (China Robot Network).

OpenAI is "considering" re-developing and manufacturing humanoid robots. According to the China Robot Network on January 2, 2025, OpenAI has recently been discussing making its own humanoid robots. Previously, OpenAI had invested in Figure and 1X as well as the "artificial general intelligence" company Physical Intelligence. (China Robot Network).

From January 7-10, 2025, CES 2025 will kick off in Las Vegas. As the world's largest, most authoritative and influential science and technology event, CES is known as the "Spring Festival Gala of Science and Technology" and is the vane of global scientific and technological innovation and consumer electronics industry. At that time, leading technology players from all over the world will showcase the most cutting-edge innovative technologies and excellent products, vividly illustrating the infinite possibilities of technology-enabled life. (Science and Technology Innovation Board Daily).

Construction machinery

China's excavator sales express in November 2024: In November 2024, 17,590 excavators of various types were sold, a year-on-year increase of 17.9%. Among them, the domestic market sales volume was 9,020 units, a year-on-year increase of 20.5%; The export volume was 8,570 units, a year-on-year increase of 15.2%. From January to November 2024, a total of 181762 excavators were sold, a year-on-year increase of 1.93%; Among them, domestic sales were 91,231 units, a year-on-year increase of 10.8%; 90,531 units were exported, a year-on-year decrease of 5.66%. (Construction Machinery Magazine).

General equipment

From January to November 2024, the operating income of China's machine tool industry was 930.2 billion yuan, a year-on-year decrease of 5.6%. Among them, metal cutting machine tools increased by 6.6% year-on-year, and metal forming machine tools increased by 5.5% year-on-year. The new orders for metal processing machine tools increased by 3.7% year-on-year, and the orders in hand increased by 4.6% year-on-year. The output of metal forming machine tools was 144,000 units, a year-on-year increase of 4.3%. The total import and export value of machine tool products was 28.79 billion US dollars, a year-on-year decrease of 1.2%. Among them, the import value was 9.19 billion US dollars, a year-on-year decrease of 9.4%; The export value was 19.59 billion US dollars, an increase of 3.2% year-on-year. the import value of metal cutting machine tools was 4.33 billion US dollars, a year-on-year decrease of 7.9%; The export value was 5.04 billion US dollars, flat year-on-year. the import value of metal forming machine tools was 620 million US dollars, a year-on-year decrease of 28.7%; The export value was 2.30 billion US dollars, an increase of 14.3% year-on-year. (China Machine Tool Industry Association).

Rail transit equipment

CRRC has recently signed a number of contracts (mainly from August to December 2024) with a total value of approximately RMB69.35 billion, including approximately RMB19.26 billion in EMU sales contracts, approximately RMB16.9 billion in EMU advanced repair contracts, approximately RMB10.4 billion in urban rail vehicle and equipment sales and maintenance contracts, and approximately RMB7.07 billion in freight vehicle sales contracts. (Company Announcement).

4. Announcements of key listed companies

【Zoomlion】Announcement on December 31, 2024: The company intends to acquire 3.39% and 0.23% of the shares of Hunan Zoomlion Intelligent Aerial Work Machinery Co., Ltd. held by Lianying Cornerstone and Xingxiang Longyin with its own funds of no more than 322.5595 million yuan and 22.5085 million yuan respectively. At the same time, the company intends to acquire 0.29% of the equity of Zoomlion held by Hunan Xingxiang Ruihang Equity Investment Partnership with its own funds of no more than 28.2179 million yuan. The acquisition of a minority stake in the holding subsidiary will help Zoomlion enhance its control over Zoomlion, improve the efficiency of operation and decision-making, and enhance the asset quality and profitability of Zoomlion.

Announcement on December 30, 2024: In order to further realize the integration of nuclear industry equipment manufacturing business and promote the high-quality development of listed companies, CNNC Suvalve Technology Industry Co., Ltd. received a notice from China National Nuclear Corporation (CNNC) that it is planning to issue shares to purchase assets and raise supporting funds and related party transactions. According to the Administrative Measures for the Material Asset Restructuring of Listed Companies and other relevant laws and regulations, this transaction is expected to constitute a major asset restructuring and a related party transaction of the company, and the reorganization will not lead to a change in the actual controller of the company. Due to the uncertainty of the relevant matters in the planning stage, in order to safeguard the interests of investors and avoid a significant impact on the company's stock price, the company's securities will be suspended from the market open on December 30, 2024 (Monday).

【Huashu Hi-Tech】12,736,547 restricted shares of the original shareholders for the initial offering 20241230 were listed and circulated. 6.79% of the outstanding shares before the lifting of the embargo; 6.35% of the outstanding shares after the lifting of the embargo; 3.08% of the total share capital.

5. Risk Warning

The macroeconomic prosperity is less than expected. The machinery industry is cyclical, and macroeconomic cyclical fluctuations may have an impact on the performance of companies in their respective industries.

Investment in fixed assets fell short of expectations. Investment in fixed assets has a greater impact on the machinery industry, and if domestic investment in fixed assets is less than expected, it may have an adverse impact on the industry.

The risk of uncertainty due to the sharp rise in raw material prices. The machinery industry is a typical manufacturing industry that requires large quantities and multiple categories of raw materials, and if the price of raw materials fluctuates significantly, it may have an impact on related companies.

Industry and market competition risks. Intensified competition in the industry will adversely affect the performance of relevant listed companies.

Risk of changes in industrial policies. The machinery industry is greatly affected by the national industrial policy, and policy changes will have an adverse impact on related industries.

Risk of third-party data errors. The data in this report is based on publicly available or purchased databases, and errors in the data published from these sources may affect the results of the analysis.

Ticker Name

Percentage Change

Inclusion Date