Transferred from: Prospective Industry Research Institute

Major listed companies in the industry: Eston (002747.SZ), Robotics (300024.SZ), Topstar (300607.SZ), EFORT (688165.SH), Inovance Technology (300124.SZ), Ecovacs (603486.SH), Roborock (688169.SH), Nine Company (689009.SH), TINAVI (688277.SH), etc

The core data of this paper: the development process of robots in China; competitive landscape of robotics market; Robotics development prospects

Industry Overview

1. Definitions

As defined by the International Organization for Standardization (ISO) ISO8373-2021, an industrial robot is an autonomously controlled, reprogrammable, multi-purpose manipulator that can be programmed on three or more axes and can be fixed in place or fixed on a mobile platform for automation applications in an industrial environment. According to the IFR (International Federation of Robotics) definition of service robots: service robots are semi-autonomous or fully autonomous robots, which can complete service work that is beneficial to human health, but does not include equipment engaged in production.

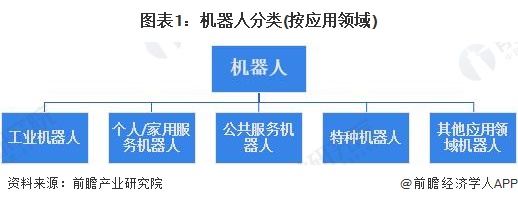

According to the classification in the "Classification of Robots" (GB/T 39405-2020) issued by the State Administration for Market Regulation and the Standardization Administration of the People's Republic of China on November 19, 2020, robots can be classified according to their application fields, and robots can be divided into industrial robots, personal/household service robots, public service robots, special robots and robots in other application fields.

2. Analysis of the industrial chain: coordinated development of upstream, midstream and downstream

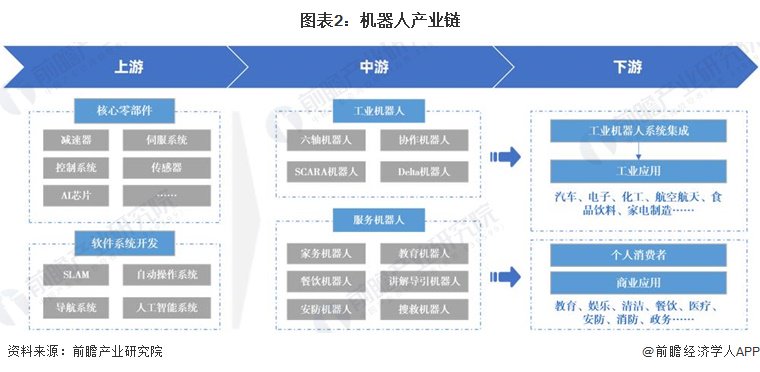

The

robot industry chain mainly develops core components and software systems, including servo systems, reducers, controllers, AI chips, sensors, etc., and software systems include artificial intelligence, SLAM, operating systems, etc.; The midstream is the manufacture of complete robots, including industrial robots and service robots; The downstream of the industrial chain is mainly oriented to end users and market applications, among which, the downstream of industrial robots is based on the specific needs of the terminal industry, which is mainly used to realize the processes or functions of welding, assembly, testing, handling, spraying, etc.; The industry applications are mainly the application of industrial robots in terminal industries with high demand for automation and intelligence, such as automobiles and electronics; The downstream of service robots are users and individual consumers in application scenarios such as education, entertainment, medical care, cleaning, security, catering, and fire protection.

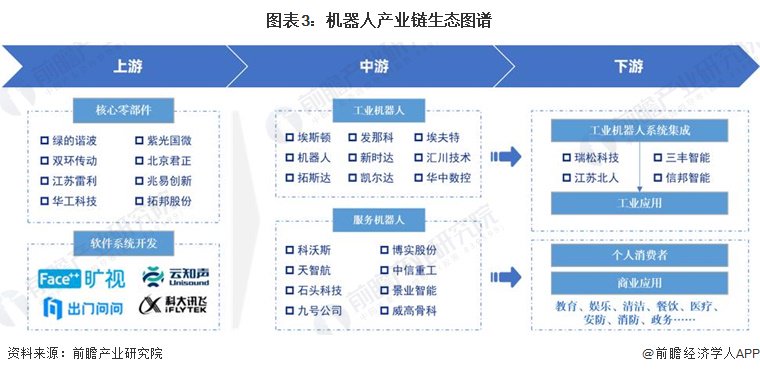

At present, the core components of the upstream of the robot industry are basically monopolized by the giants of international robot manufacturers, such as green harmonics, double-ring transmission, Ziguang Guowei, etc., and representative software system enterprises such as iFLYTEK, TZTEK Technology, Yuncong Technology, etc.; The representative enterprises of industrial robots in the middle of the industrial chain include Estun, SIASUN Robotics, Topstar, etc., and the representative enterprises of service robots include Ecovacs, TINAVI, Roborock, etc.; Representative enterprises of downstream industrial robot system integration include Ruisong Technology, Jiangsu Beiren, etc., with rich application scenarios and a wide range of application fields and a large number of enterprises.

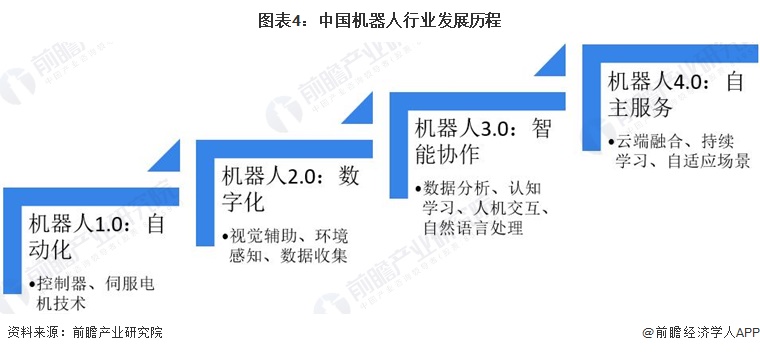

Industry history: 4.0 era

In 2017, the China Academy of Information and Communications Technology, IDC International Data Group and Intel jointly released the white paper "Robot 3.0 New Ecology in the Era of Artificial Intelligence", which divides the development process of robots into three eras, which are called robot 1.0, robot 2.0 and robot 3.0. In 2019, Intel and a number of companies released the "Robot 4.0 White Paper" (hereinafter referred to as the "White Paper") and made a prediction that robots will enter the 4.0 era in 2020. According to the definition of the white paper, in the 4.0 era, the "cloud brain" of the robot will be distributed in various places from the cloud to the end, and will make full use of edge computing to provide more cost-effective services, and combine the memory scenarios to complete the task with common sense to achieve large-scale deployment.

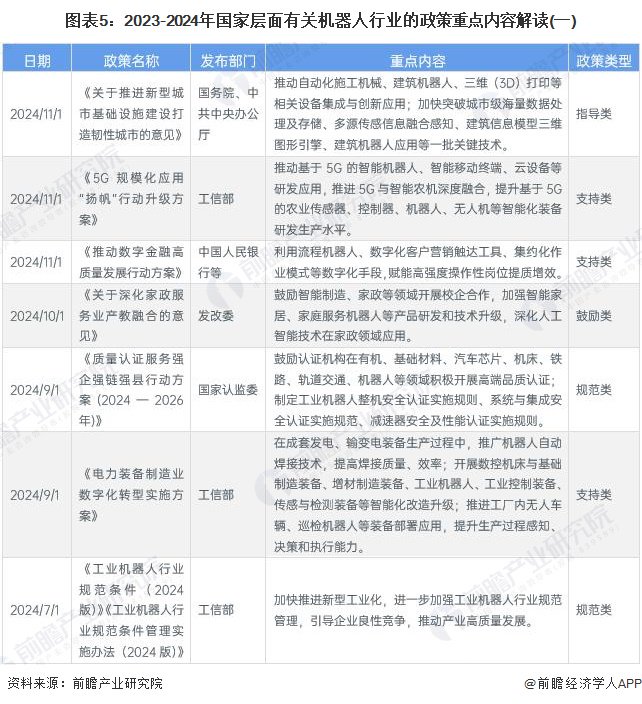

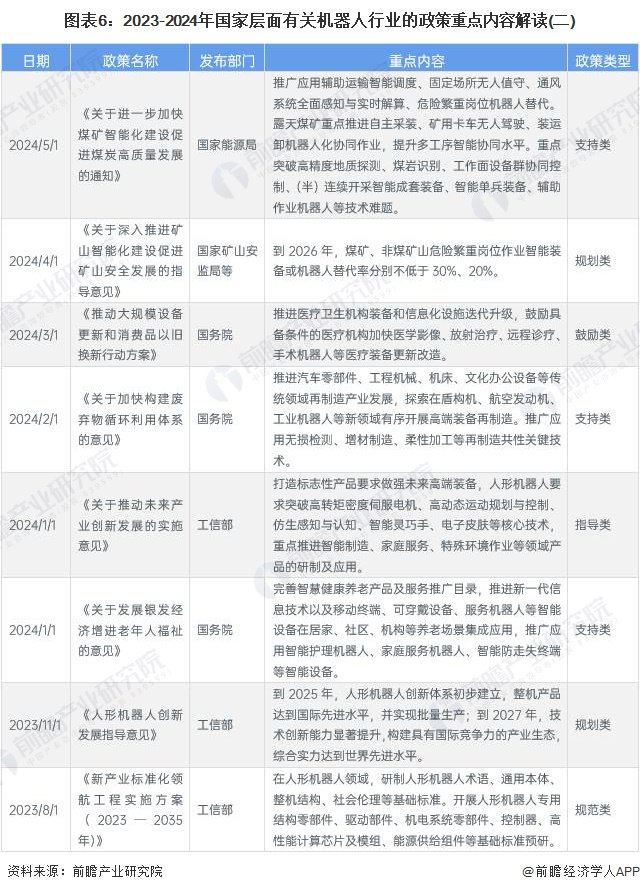

Industry development policy background: promote industrial transformation and upgrading

In recent years, the government has adopted a series of policy measures to support the development of the robot industry, such as supporting the research and development and application of robot technology, investment and financing policies to support the development of the robot industry, and policy measures to vigorously develop the emerging industry of robots. These policies and measures will help promote the development of the robot industry, and the relevant policies and regulations and the main contents are shown in the following table

China's industry development

1. The output of robots continues to grow

Since 2021, as China takes the lead in recovering from the epidemic, industrial robots have ushered in the double benefits of the domestic market and the international market; In 2023, China's industrial robot output will be 429,500 units; From January to November 2024, China's industrial robots will be produced in a total of 483,900 units, a year-on-year increase of 11%.

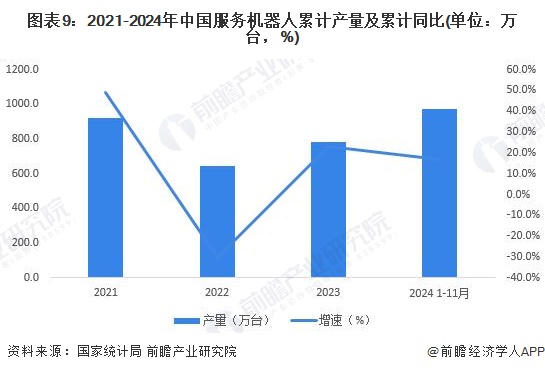

According to the data provided by the National Bureau of Statistics, 2021 is a year of explosive growth for China's service robot industry, with an annual output of 9,214,400 units, a year-on-year increase of 48%; In 2023, the cumulative output of service robots will increase by 23.3%; From January to November 2024, the cumulative output of service robots increased by 17% year-on-year. On the whole, China's service robot industry has been developing rapidly in recent years.

2. The overall number of industrial robot installations has increased

The

development of the industrial robot market is mainly due to the upgrading of China's manufacturing industry and the increase in automation demand, especially in the automobile manufacturing, electronic and electrical, metal processing and other industries. According to IFR data, the annual installation of industrial robots in China in 2023 will be 276,300 units, a year-on-year decrease of 5%; From 2018 to 2023, the compound annual growth rate of industrial robot installation will reach 12%.

3. The robot market size exceeds 130 billion yuan

The demand for intelligent transformation and upgrading of China's manufacturing is becoming increasingly prominent, and the market demand for industrial robots is strong, and it is the world's largest industrial robot application market. The development of China's service robot industry started relatively late compared with the United States, Japan and other countries, but due to factors such as population aging, the market scale has been expanding in recent years. Overall, the market size of China's robot industry is generally showing a trend of rapid growth, with the overall scale exceeding 130 billion yuan in 2023, a year-on-year increase of 19.6%.

Analysis of China's industry competition landscape

1. Regional competition: Shandong Province has the largest number of enterprises

As of December 19, 2024, Shandong Province has the largest number of robot manufacturing enterprises at 2,371, followed by Guangdong Province, Jiangsu Province, Zhejiang Province, Anhui Province and Hebei Province.

Note: As of December 19, 2024.

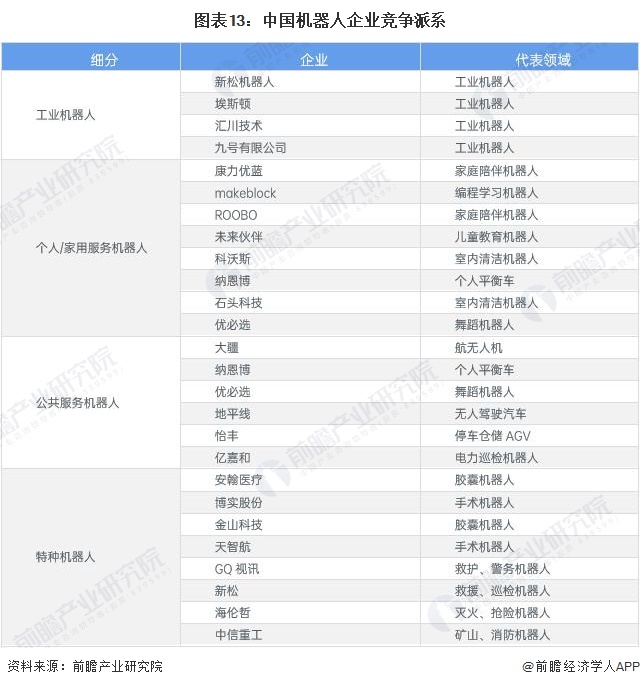

2. Enterprise competition: diversified competition

In the competitive landscape of the robot industry, various subdivisions show a diversified competitive situation. In the field of industrial robots, SIASUN Robot, Estun and other companies focus on industrial production optimization, improve efficiency and precision, and occupy most of the market share by virtue of technology accumulation; In terms of personal/household service robots, Ecovacs, Roborock and other companies continue to launch new products to expand market boundaries; In the field of public service robots, companies such as DJI and Horizon Robotics have made use of their technological advantages to play an effective role in aerial photography, transportation and other scenarios to help the construction of smart cities. In the field of special robots, Anhan Medical, CITIC Heavy Industries and other enterprises have developed suitable products for specific industry needs to ensure operation safety and efficiency. On the whole, the enterprises of each faction are deeply engaged in their respective fields with technology, positioning and innovation capabilities, promoting the diversified and intelligent development of China's robot industry, and building an industrial ecosystem.

Industry development prospects

With the deepening of the domestic substitution of servo motors and harmonic reducers, the demand side is large, the low-end market of industrial robots will grow strongly, and the technological breakthroughs of domestic brands in the mid-to-high-end market will account for more share, and the market scale will grow rapidly. At the same time, the development of technology to promote the demand for service robots to increase, the market is growing rapidly and gradually opening, China's service robots are about to enter the start-up period, the future market will continue to expand. On the whole, it is expected that in the next few years, China's robot industry will maintain a rapid growth trend, from 2024 to 2029, the compound annual growth rate of the robot market is about 21%, and by 2029, the robot market size is expected to exceed 410 billion yuan.

For more research and analysis of this industry, please refer to the "China Robot Industry Market Prospect and Investment Strategic Planning Analysis Report" of the Prospective Industry Research Institute

At the same time, the Prospective Industry Research Institute also provides solutions such as industrial new track research, investment feasibility study, industrial planning, park planning, industrial investment, industrial map, industrial big data, smart investment promotion system, industry status certificate, IPO consulting/fundraising feasibility study, specialized and special new small giant declaration, and the 15th Five-Year Plan. If you want to reprint and quote the content of this article, please indicate the source (Qianzhan Industry Research Institute).

More in-depth industry analysis is available in the [Prospective Economist APP], and you can also communicate and interact with 500+ economists/senior industry researchers. More enterprise data, enterprise information, and enterprise development are all in the [Qichamao APP], the most cost-effective and most comprehensive enterprise query platform.

Ticker Name

Percentage Change

Inclusion Date