Transferred from: Prospective Industry Research Institute

Major listed companies in the industry: Ecovacs (603486), Roborock (688169), Robotics (300024), Nine Company (689009), Boshi (002698), TINAVI (688277), Jingye Intelligent (688290), Yijiahe (603666), etc

The core data of this paper: service robot industry chain; the size of the service robot market; the development trend of service robots, etc

Industry Overview

1. Definitions

According to the definition of a robot in the Glossary of Robots and Robot Equipment (GB/T 12643-2013), a robot is an actuator with two or more programmable axes and a certain degree of autonomy that can move within its environment to perform a predetermined task.

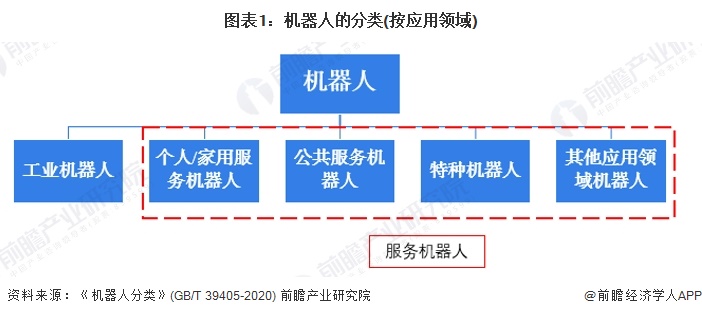

Classified according to the application field of robots, robots can be divided into industrial robots, personal/household service robots, public service robots, special robots, and other application field robots. According to the definition of the Glossary of Robots and Robot Equipment (GB/T 12643-2013), a service robot refers to a robot that can complete useful tasks for humans or equipment except for industrial automation applications.

2. Analysis of the industrial chain: across multiple technical fields and the technical barriers of each link are high

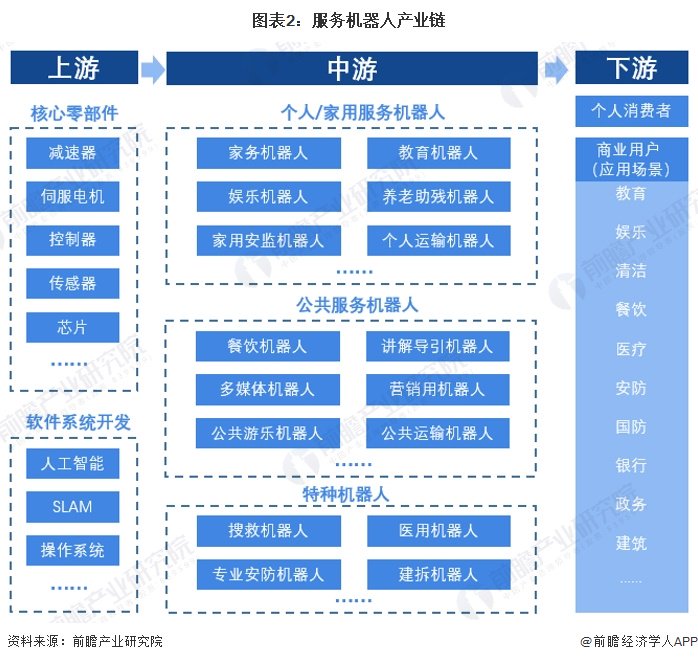

From the perspective of the industrial chain, the service robot industry can be divided into the development of core components and software systems in the upstream, the ontology manufacturing of service robots in the midstream, individual consumers in the downstream and commercial users in various application scenarios. The technology involved in the service robot industry chain spans many high-tech fields such as communication and artificial intelligence, and the technical barriers in each link are high.

In the upstream hardware part, the reducer, the servo motor for the robot, and the controller are the three core components of the service robot. As service robots pay more attention to intelligence and humanization, core components such as AI chips and sensors are equally important. In the upstream software system development part, artificial intelligence, SLAM, operating system and other software and systems that make up service robots.

In the middle of the industrial chain, the ontology manufacturing of service robots is mainly divided into three categories: personal/household service robots, public service robots, and special robots. The downstream is for users and individual consumers in application scenarios such as education, entertainment, medical care, cleaning, security, catering, and fire protection.

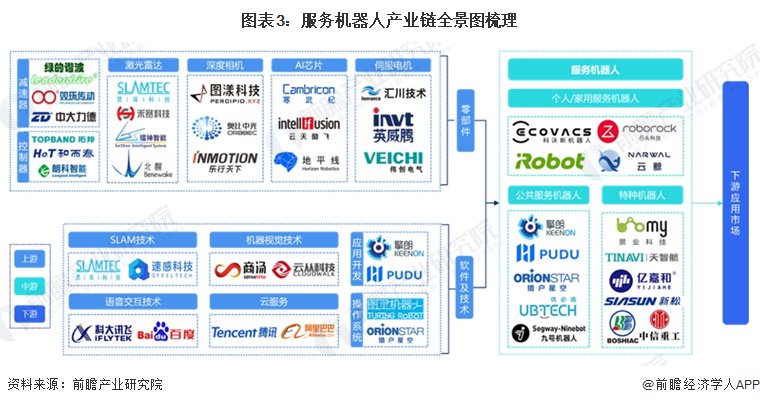

From the perspective of representative enterprises in each link of the industrial chain, the upstream is mainly component suppliers such as Green Harmonic, Heertai, Hesai Technology, and Obi Zhongguang, technical service providers such as Silan Technology, SenseTime, and iFLYTEK, as well as cloud computing service providers such as Alibaba and Tencent; Midstream service robot companies mainly include personal/home service robot manufacturers such as Ecovacs and Roborock, public service robot manufacturers such as Keenon Intelligence, Pudu Technology, and Orion Star, as well as special service robot manufacturers such as Jingye Intelligence and Yijiahe.

Industry development history: in a period of rapid development

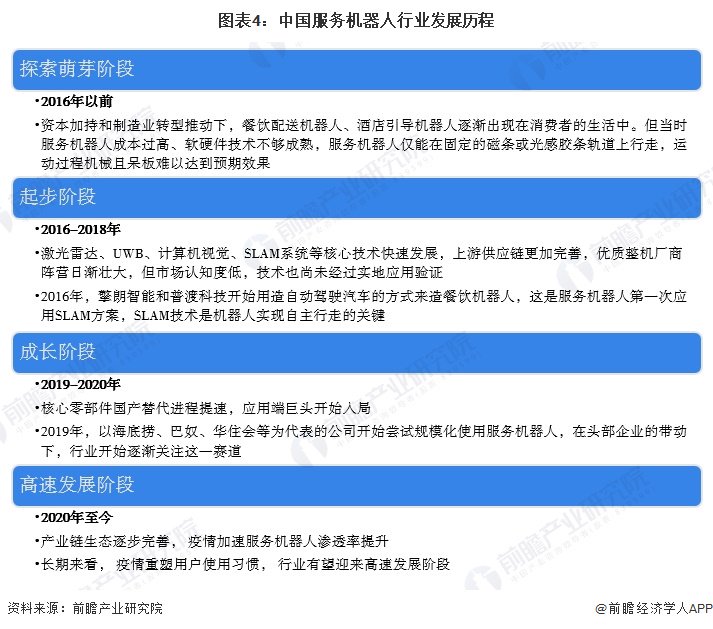

China's service robot industry started late, and the core components such as lidar and depth cameras mainly relied on imports in the early stage, and the development level of key technologies such as SLAM was also low. In recent years, with the acceleration of the localization process of core hardware and the acceleration of iterative upgrading of key intelligent technologies, the pace of commercial application of service robots has been accelerating; At the same time, as the application giants began to enter the market and the epidemic accelerated the digital transformation, the value of the service robot industry has been continuously highlighted, the penetration rate has accelerated, and the industry has now entered a stage of rapid development.

Industry policy background: policy support to help the high-quality development of the service robot industry

Robots are an important indicator of a country's ability to innovate. In recent years, the state has successively introduced a number of policies to encourage the development and innovation of the service robot industry, the "14th Five-Year Plan" robot industry development plan, "robot +" application action implementation plan, "on the development of silver economy to enhance the well-being of the elderly" and other policies on the development direction of service robots, application fields and technical priorities and other aspects of planning and requirements, intended to enhance the key technological innovation capabilities of service robots, improve the product guarantee ability and quality and efficiency level of service robots, Promote the high-quality development of the service robot industry.

Industry development

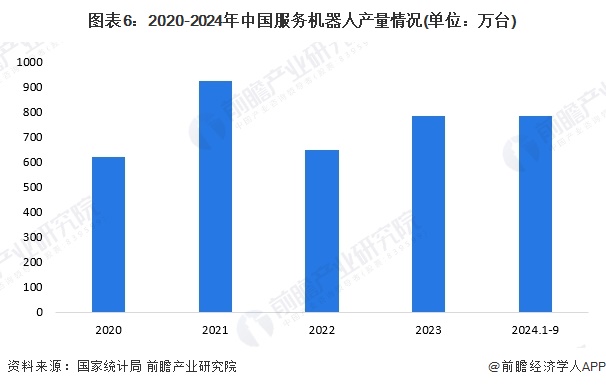

1. The output of service robots fluctuates and grows

In recent years, the output of domestic service robots has grown rapidly. According to the data disclosed by the National Bureau of Statistics, from 2020 to 2023, the output of China's service robots will fluctuate and grow, of which 2021 will be a year of explosive growth in China's service robot industry, with an annual output of 9.2144 million units, a year-on-year increase of 48%. In 2023, the national output of service robots will be 7.833 million units, although it will decrease compared with 2021, it will still remain at a high level. From January to September 2024, the national output of service robots will reach 7.834 million units, which has exceeded the annual output in 2023.

Note: The National Bureau of Statistics began to disclose data related to the production of service robots in 2021, and the data for 2020 is derived backwards based on the growth rate

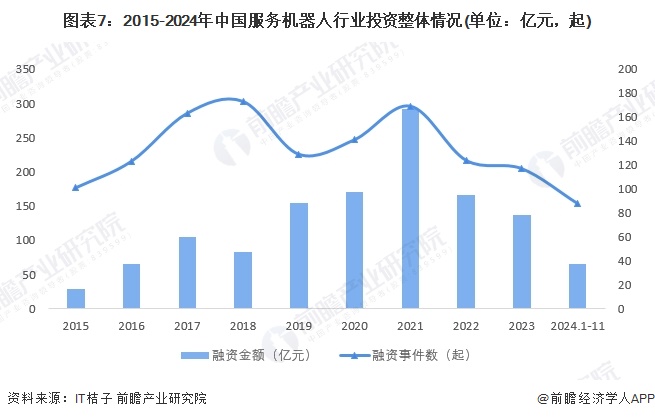

2. The industry investment is hot

According to the statistics of IT oranges, from 2015 to 2023, the amount of investment and the number of investment events in the field of service robots in China are generally increasing. The investment amount has grown rapidly since 2015 and peaked in 2021, with a total of 169 investment events and a total investment amount of 29.243 billion yuan. From 2015 to 2023, a total of 1,240 investment events occurred, with an investment amount of 120.25 billion yuan.

Note: The data comes from the "Service Robot" tab in the IT Orange Investment Event Database, and the statistics are as of November 8, 2024

3. The market scale of service robots continues to expand

In recent years, China's service robot market has grown rapidly, and the demand for medical care, education, public services and other fields has become the main driving force. According to LiveReport's "2024 White Paper on the Development of Artificial Intelligence Industry in Hong Kong Stocks", the size of China's service robot market will reach RMB 66 billion in 2023, a year-on-year increase of 27.9%.

The competitive landscape of the industry

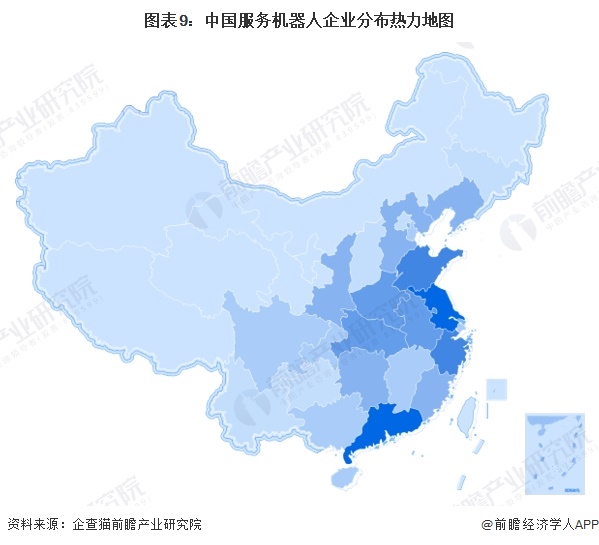

Regional competition: Guangdong and Jiangsu are the most concentrated

From the perspective of the regional distribution of service robot industry chain enterprises, the distribution of service robot enterprises in China is relatively concentrated, mainly distributed in the economically developed eastern coastal areas, represented by Guangdong Province, Jiangsu Province, Shandong Province and Zhejiang Province. The number of service robot enterprises in the western region is relatively small.

Enterprise competition: The layout of service robot enterprises has its own focus

A service robot is a robot that can perform useful tasks for humans or equipment in addition to industrial automation applications. Due to the different needs of products, the difference between service robot products in different fields is greater, so the competitors in the market segmentation market are also very different, from the perspective of the competition of major products in the industry, sweeping robot enterprises mainly include Ecovacs, Rock Technology, etc.; In the field of catering robots, Keenon Intelligence, Orion Star, Pudu Technology, etc. are the main players in China; The main participating companies of medical robots include TINAVI, Anhan Technology, Weigao Orthopedics, etc.; In the security robot market, the main participating companies are CITIC Heavy Industries, Guozi Robots, etc.

Industry development prospects and trend forecasts

1. The market size will exceed 180 billion yuan in 2029

Driven by the support of national industrial policies, the gradual maturity of technical conditions and the release of downstream consumer demand, the scale of China's service robot market is expected to continue to rise from 2024 to 2029, and the market size will exceed 180 billion yuan in 2029, with a compound annual growth rate of 18.6% from 2024 to 2029.

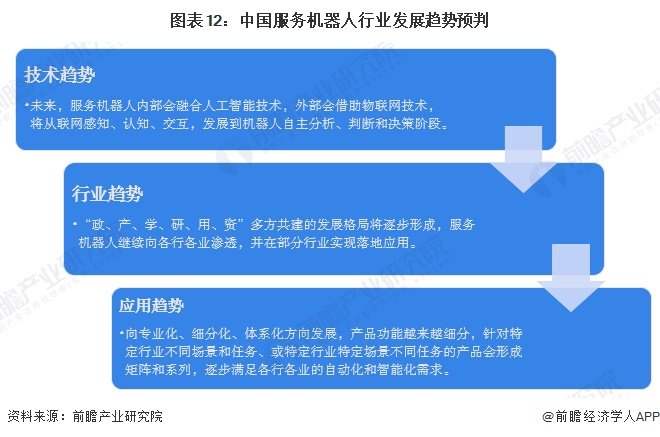

2. The penetration rate of the industry is gradually increasing, and it is moving towards intelligence and specialization

Technologies represented by artificial intelligence, cloud computing, and the Internet of Things will drive the service robot industry to move rapidly towards intelligence, innovation, and digitalization. In the future, service robots are expected to become the entrance and connector of scene data, and an important link to realize the integration of full-scene digitalization and cloud-edge-end collaboration. With the advancement of the national strategy and the development of the industrial chain, more and more organizations and individuals will participate in the service robot industry, and the development pattern of "government, industry, learning, research, use, and capital" will gradually take shape, and the service robot will continue to penetrate into all walks of life, and realize the application in some industries.

The industrial chain of service robots will gradually improve, technological innovation achievements will gradually accumulate, the industry will become more large-scale and systematic, the processing capacity in specific businesses will become more and more professional, and the product functions will become more and more subdivided.

For more research and analysis of this industry, please refer to the "Market Prospect and Investment Strategic Planning Analysis Report of China's Service Robot Industry" by the Prospective Industry Research Institute

At the same time, the Prospective Industry Research Institute also provides solutions such as industrial new track research, investment feasibility study, industrial planning, park planning, industrial investment, industrial map, industrial big data, smart investment promotion system, industry status certificate, IPO consulting/fundraising feasibility study, specialized and special new small giant declaration, and the 15th Five-Year Plan. If you want to reprint and quote the content of this article, please indicate the source (Qianzhan Industry Research Institute).

More in-depth industry analysis is available in the [Prospective Economist APP], and you can also communicate and interact with 500+ economists/senior industry researchers. More enterprise data, enterprise information, and enterprise development are all in the [Qichamao APP], the most cost-effective and most comprehensive enterprise query platform.

Ticker Name

Percentage Change

Inclusion Date